health /

What is the minimum score for an FHA loan?

Minimum FHA loan credit score requirement

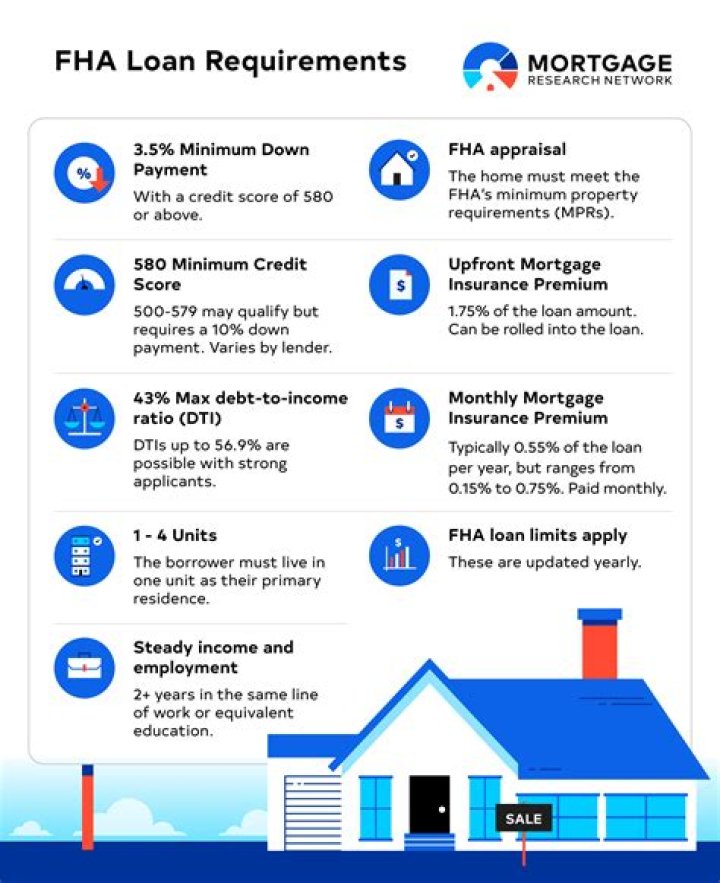

The minimum credit score to qualify for an FHA loan is 580 with a down payment of 3.5 percent. If you can bump up your down payment to at least 10 percent, you can have a credit score as low as 500 and still qualify.Can I buy a house with a 580 credit score?

Most lenders offer FHA loans starting at a 580 credit score. If your score is 580 or higher, you need to pay only 3.5% down. Those with lower credit (500-579) may still qualify for an FHA loan. But you'd need to put at least 10% down, and it can be harder to find lenders that allow a 500 minimum credit score.What will disqualify you from an FHA loan?

There are three popular reasons you have been denied for an FHA loan–bad credit, high debt-to-income ratio, and overall insufficient money to cover the down payment and closing costs.Is FHA hard to get?

Here's the bottom line. It's not necessarily easy to qualify for an FHA loan. You have to be a fairly well-qualified borrower. But it might not be as hard as getting a conventional mortgage, due to the government insurance we talked about earlier.Which credit score do FHA lenders use?

2 Answers. Lenders work with what's called a "representative" credit score. They will pull a report that includes two or three scores from TransUnion, Experian, and / or Equifax. When there are two scores, the lower score is considered "representative." If there are three, it's the middle score.What is the Minimum Credit Score for an FHA Loan?

Does FHA look at Equifax or TransUnion?

FHA loan rules provide clear instructions for the lender when it comes to verifying your ability to afford a home loan. Lenders look at the credit reports in your name at the three major credit reporting agencies; TransUnion, Equifax, and Experian.How big of a loan can I get with a 650 credit score?

Lenders will usually offer an FHA loan to someone with a credit score as low as 500, as long as they can put down 10%. With a credit score above 580, you could qualify for a down payment as low as 3.5%.Why do sellers not want FHA loans?

Reasons Sellers Don't Like FHA LoansBoth reasons have to do with the strict guidelines imposed because FHA loans are government-insured loans. For one, if the home is appraised for less than the agreed-upon price, the seller must reduce the selling price to match the appraised price, or the deal will fall through.

How long does it take for an FHA loan to get approved?

FHA loans take about the same amount of time to be processed as a conventional or VA loan, approximately 45 days. That includes the entire process, from the loan application to the final approval and closing.Is it better to go FHA or conventional?

A conventional loan is often better if you have good or excellent credit because your mortgage rate and PMI costs will go down. But an FHA loan can be perfect if your credit score is in the high-500s or low-600s. For lower-credit borrowers, FHA is often the cheaper option.How often do FHA loans get denied?

In 2020, 9.3% of applicants were denied a home-purchase loan, according to data collected under the Home Mortgage Disclosure Act. However, some loan programs have a higher denial rate than others. Here's how it breaks down. Federal Housing Administration loans: 14.1% denial rate.Can I get a FHA loan with collections on my credit report?

FHA guidelines stipulate that you do not have to pay any non-medical collections that are on your credit report if their combined total is less than $2,000. However, those collections may count towards your debt to income ratio. As a result, you may need to pay some or all of these to qualify for your FHA loan.What are the new FHA guidelines?

FHA loan limitsFHA mortgage limits vary by county and the number of housing units. The FHA loan limit in 2022 for one-unit properties in low-cost areas is $420,680. Single-unit homes in higher-cost areas can have a maximum limit as high as $970,800 for calendar year 2022.

How can I raise my credit score 50 points fast?

Here are some strategies to quickly improve your credit:

- Pay credit card balances strategically.

- Ask for higher credit limits.

- Become an authorized user.

- Pay bills on time.

- Dispute credit report errors.

- Deal with collections accounts.

- Use a secured credit card.

- Get credit for rent and utility payments.