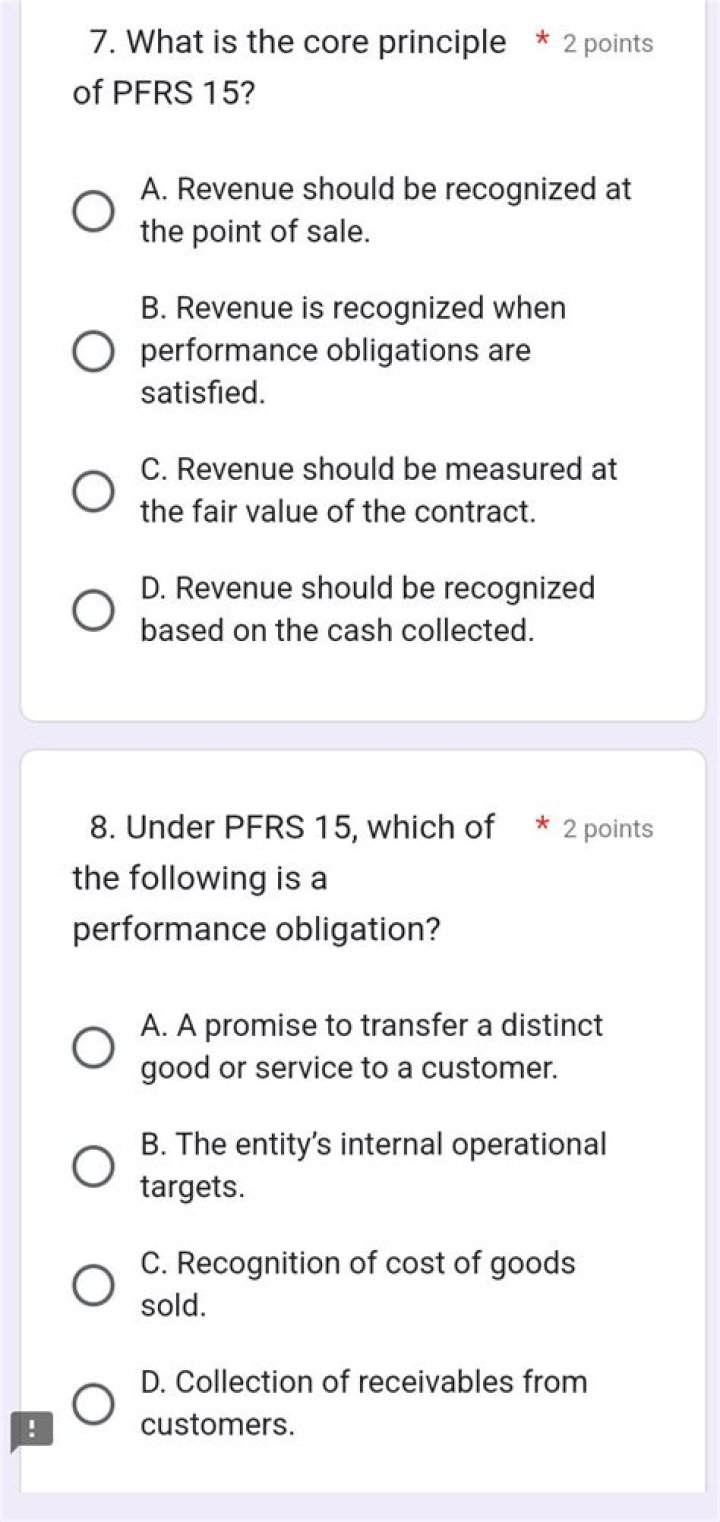

What is the core principle of Pfrs 15?

The core principle of IFRS 15 is that revenue is recognised when the goods or services are transferred to the customer, at the transaction price.

What types of revenue IFRS 15 covers with regard to revenues from contracts with customers?

IFRS 15 Revenue from contracts with customers

- The sale of goods.

- The rendering of service; and.

- The use by others of enterprise assets yielding: interest, royalties or dividends.

Who does Pfrs 15 affect?

One of those industries that will be affected by PFRS 15 is the real estate industry. PFRS 15 requires the application of significant judgment in some areas, but in other areas it is relatively prescriptive, allowing little room for judgment.

Does IAS 18 still apply?

This Standard will apply to annual periods beginning or after 1 Jan 2018, and will replace IAS 11 Construction Contracts and IAS 18 Revenue. The new Standard will apply to all contracts with customers except for leases, financial instruments and insurance contracts, which are covered by other accounting standards.

What are the five key steps a company follows to apply the core revenue recognition principle?

The five steps needed to satisfy the updated revenue recognition principle are: (1) identify the contract with the customer; (2) identify contractual performance obligations; (3) determine the amount of consideration/price for the transaction; (4) allocate the determined amount of consideration/price to the contractual …

What are the steps for revenue recognition in contracts?

IFRS 15, revenue from contracts with customers, establishes the specific steps for revenue recognition. It is important to note that there are some exclusions from IFRS 15 such as: The five steps for revenue recognition in contracts are as follows:

What makes up the revenue of a contract?

Customer-furnished materials The value of goods or services contributed by a customer (for example, materials, equipment, or labour) to facilitate the fulfilment of the contract is included in contract revenue (as non-cash consideration) if the entity controls these goods or services after they are provided.

What are the steps for revenue recognition in IFRS 15?

IFRS 15, revenue from contracts with customers, establishes the specific steps for revenue recognition. It is important to note that there are some exclusions from IFRS 15 such as: The five steps for revenue recognition in contracts are as follows: 1. Identifying the Contract All conditions must be satisfied for a contract to form:

When is a contract in the scope of IFRS 15?

IFRS 15.9 A contract with a customer is in the scope of the standard when it is legally enforceable and meets all of the following criteria.