What is recorded in the purchases account?

The purchases account is a general ledger account in which is recorded the inventory purchases of a business. This account is used to calculate the amount of inventory available for sale in a periodic inventory system.

What does purchase discount mean in accounting?

Purchase discount is an offer from the supplier to the purchaser, to reduce the payment amount if the payment is made within a certain period of time. Under the gross method, the total cost of purchases are credited to accounts payable first, and discounts realized later if the payments were made in time.

What type of account is purchases discount?

Companies that take advantage of sales discounts usually record them in an account named purchases discounts, which is another contra‐expense account that is subtracted from purchases on the income statement.

What does it mean to use a purchase discount account?

12) The use of a Purchase Discounts account implies that the recorded cost of a purchased inventory item is its invoice price less the purchase discount taken. invoice price less the purchase discount allowable whether taken or not. invoice price plus any purchase discount lost.

Where does the purchase discount go on the income statement?

The purchases discounts normal balance is a credit, a reduction in costs for the business. The discount is recorded in a contra expense account which is offset against the appropriate purchases or expense account in the income statement. Purchase Discount Not Taken

Is there an inventory account in purchase discount journal entry?

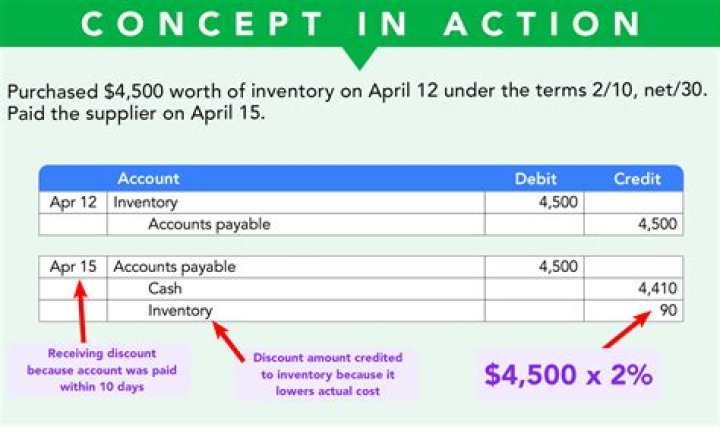

Hence, there is no inventory account in the above journal entry. Under perpetual inventory system, the company can make the purchase discount journal entry by debiting accounts payable and crediting cash account and inventory account. In this journal entry, there is no purchase discount account like in the periodic inventory system.

What happens to purchase discounts at the end of the period?

In this journal entry, the purchase discounts is a temporary account which will be cleared to zero at the end of the period. Its normal balance is on the credit side and will be offset with the purchases account when the company calculates cost of goods sold during the accounting period.