How do you account for insurance in accounting?

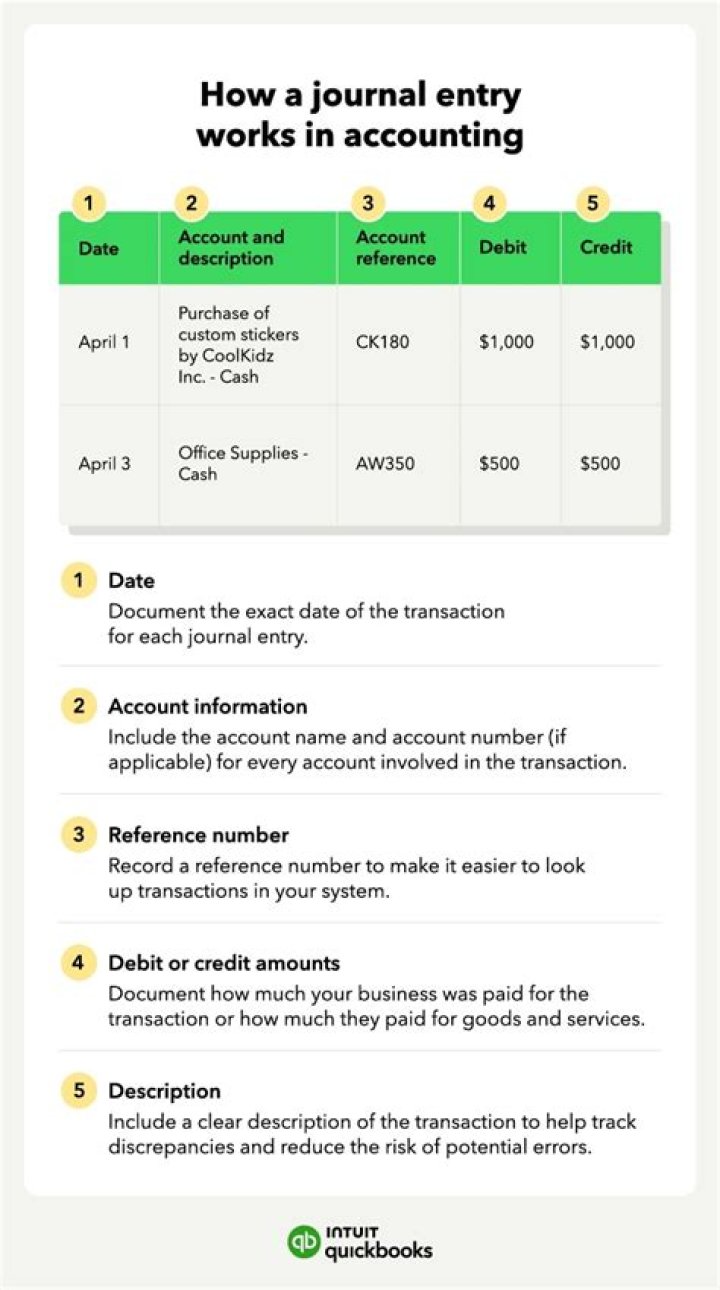

Prepaid Insurance Journal Entry When the asset is charged to expense, the journal entry is to debit the insurance expense account and credit the prepaid insurance account. Thus, the amount charged to expense in an accounting period is only the amount of the prepaid insurance asset ratably assigned to that period.

Do insurance companies need accountants?

All insurance companies are required to use statutory accounting when preparing their financial statements because of the risky nature of the industry.

What type of account is insurance in accounting?

Account Types

| Account | Type | Debit |

|---|---|---|

| INSURANCE EXPENSE | Expense | Increase |

| INSURANCE PAYABLE | Liability | Decrease |

| INTEREST EXPENSE | Expense | Increase |

| INTEREST INCOME | Revenue | Decrease |

What is SSAP accounting?

SSAP, or Statements of Standard Accounting Practice, are edicts by which trading companies that are listed on the stock market must adhere to when constructing their financial reports. They form part of the Generally Accepted Accounting Practice, or GAAP, which is statutory in the United Kingdom through the Taxes Acts.

What is the journal entry for insurance?

A basic insurance journal entry is Debit: Insurance Expense, Credit: Bank for payments to an insurance company for business insurance. Not all insurance payments (premiums) are deductible* business expenses. Some insurance payments can go on to the Profit and Loss Report and some must go on the Balance Sheet.

What do accountants do at insurance companies?

He or she is responsible for managing all types of accounts for an insurance broker, including accounts receivable, payroll, investments, pool management, and claims. An insurance accountant may also be responsible for performing audits on the departments in the insurance brokerage house.

What is the difference between GAAP and stat accounting?

Statutory Accounting Principles, also known as SAP, are used to prepare the financial statements of insurance companies. On the other hand, Generally Accepted Accounting Principles or GAAP provides a common set of accounting standards, procedures and rules that are defined by the professional accountancy body.

Are there accounting practices in property and casualty insurance?

After reviewing hundreds of financial statements of property and casualty (P&C) insurance agencies, we have found that accountants often do not understand how agencies operate, which can lead to misleading and often inaccurate accounting practices.

Who is the American Property Casualty Insurance Association?

American Property Casualty Insurance Association The American Property Casualty Insurance Association (APCIA) is the primary national trade association for home, auto, and business insurers. APCIA promotes and protects the viability of private competition for the benefit of consumers and insurers, with a legacy dating back 150 years.

How to start an independent property and casualty insurance agency?

Starting an independent Property and Casualty Insurance agency can be daunting. Where do I start? How will I get licensed, find insurance companies that I can represent, and open an office?

Why do you need property and casualty insurance?

Property insurance protects property in the case of damage or theft, or protects the owner if someone is injured on their property. Casualty insurance helps protect individuals from liability if they are responsible for damaging another person’s property or causing an accident that resulted in injuries to another person.